THE PRICE OF AN HOUR AT THE TOP

Prism · Executive Compensation

SEC Filings · January 2025

THE PRICE

OF AN HOUR

AT THE TOP

Tesla CFO Vaibhav Taneja earned $48,767 per hour — $35,000 more per hour than Alphabet's CFO in second place. Amy Hood at Microsoft earned $10,308/h. The CFO of Alphabet nearly $13,500/h. These figures, derived from total SEC-reported compensation divided by a 55-hour work week, reveal the extraordinary concentration of financial reward at the top of America's largest companies and the extent to which one-time equity awards can create outliers that dwarf even their well-compensated peers.

Methodology: Total compensation from SEC filings (latest fiscal year) ÷ 55-hour work week × 52 weeks

Scope: CFOs of the 50 biggest U.S. companies · Mid-year changes prorated

Outlier: Tesla's Vaibhav Taneja $48,767/h — board awarded large one-time stock package on promotion to CFO

Source: SEC Filings · Markets in a Minute · As of January 14 2025

Scope: CFOs of the 50 biggest U.S. companies · Mid-year changes prorated

Outlier: Tesla's Vaibhav Taneja $48,767/h — board awarded large one-time stock package on promotion to CFO

Source: SEC Filings · Markets in a Minute · As of January 14 2025

Prism Desk·Source: SEC Filings·January 14 2025

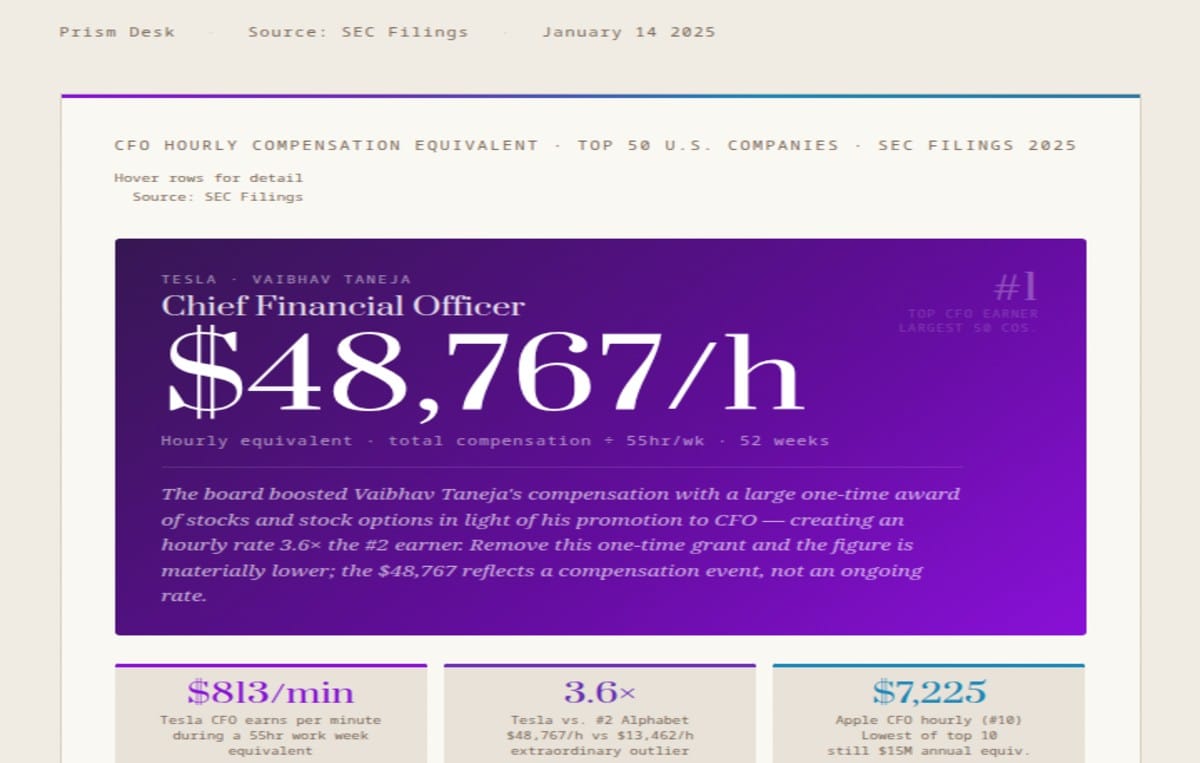

CFO Hourly Compensation Equivalent · Top 50 U.S. Companies · SEC Filings 2025

Hover rows for detail

Source: SEC Filings

Source: SEC Filings

#1Top CFO earner

largest 50 cos.

Tesla · Vaibhav Taneja

Chief Financial Officer

$48,767/h

Hourly equivalent · total compensation ÷ 55hr/wk · 52 weeks

The board boosted Vaibhav Taneja's compensation with a large one-time award of stocks and stock options in light of his promotion to CFO — creating an hourly rate 3.6× the #2 earner. Remove this one-time grant and the figure is materially lower; the $48,767 reflects a compensation event, not an ongoing rate.

largest 50 cos.

$813/min

Tesla CFO earns per minute

during a 55hr work week

equivalent

during a 55hr work week

equivalent

3.6×

Tesla vs. #2 Alphabet

$48,767/h vs $13,462/h

extraordinary outlier

$48,767/h vs $13,462/h

extraordinary outlier

$7,225

Apple CFO hourly (#10)

Lowest of top 10

still $15M annual equiv.

Lowest of top 10

still $15M annual equiv.

How the hourly figure is calculated: Total compensation from SEC proxy filings (including base salary, cash bonus, stock awards, option awards, and other compensation) is divided by a 55-hour work week × 52 weeks = 2,860 hours/year. For CFOs who changed mid-year, compensation was prorated. Stock awards are valued at grant-date fair value — the actual realised value depends on share price movement after the grant. A large one-time equity award at promotion, as in Taneja's case, creates a single-year compensation spike that will not recur in future years at the same magnitude.

Excluding Tesla outlier — #2 through #10 · true peer range

Tesla Outlier$48,767One-time promotion equity

3.6× the #2 earner

Not a recurring rate

3.6× the #2 earner

Not a recurring rate

Tech CFO Range$7–13K/hAlphabet · Microsoft · Amazon

Cisco · Meta · Netflix

NVIDIA · Apple

Cisco · Meta · Netflix

NVIDIA · Apple

Financial Sector$7,370/hGoldman Sachs Denis Coleman

Finance CFOs vs tech

Similar order of magnitude

Finance CFOs vs tech

Similar order of magnitude

Equity vs. cash reality: The hourly figures are dominated by stock and option awards — base salaries for CFOs at this level typically run $500K–$2M annually, translating to roughly $175–$700/hour. The $7,000–$48,000 ranges reflect equity grant-date valuations. An executive who receives $80M in stock options whose underlying shares subsequently fall 30% realised far less than the reported figure. The SEC-required grant-date fair value disclosure is a standardised accounting measure, not a guarantee of actual remuneration received.

Source: SEC Proxy Filings · Markets in a Minute · Based on total compensation in latest fiscal year assuming 55hr work week · As of January 14 2025

$48,767Tesla CFO

Hourly Rate (#1)

Hourly Rate (#1)

$13,462Alphabet CFO

Hourly Rate (#2)

Hourly Rate (#2)

3.6×Tesla Premium

vs. #2 Alphabet

vs. #2 Alphabet

$7,225Apple CFO (#10)

Still $15M+/year

Still $15M+/year

The Hourly Illusion and the Annual Reality

The practice of converting annual executive compensation to an hourly rate — total SEC-reported pay divided by a 55-hour work week over 52 weeks — produces figures that are simultaneously literally accurate and contextually misleading in ways worth unpacking. Tesla CFO Vaibhav Taneja's $48,767 per hour is a true arithmetic statement about his total reported compensation for a fiscal year that included a large one-time equity grant on his promotion to CFO, divided by a full year's assumed hours. But it is not a description of what he receives per hour of work in any meaningful ongoing sense — it is a description of a compensation event that produced a single-year anomaly.

The hourly framing is useful precisely because it makes the abstract concrete: most people can relate to an hourly wage in a way that they cannot relate to a $278 million total compensation package. The $48,767 hour converts an accounting number into a human-scale reference point — approximately what a median American household earns in a year, concentrated into 60 minutes of one man's working time. Whether this framing illuminates or distorts depends on how much weight one places on the annual total versus the per-unit-of-time framing, and on whether one accepts the 55-hour work week assumption as a reasonable denominator.

$48,767 an hour. $813 a minute. More than a median American household earns in a year, every hour, for 2,860 hours a year. The number is accurate. The comparison is legitimate. What it reveals about the structure of executive compensation is uncomfortable regardless of one's views on its justification.

Why Tesla's Figure Is an Outlier Even Among Outliers

The 3.6× gap between Tesla's Vaibhav Taneja ($48,767/h) and Alphabet's Ruth Porat / Anat Ashkenazi ($13,462/h) is more than the gap between Alphabet and every other company in the top 10. This extreme outlier status reflects the specific dynamics of equity compensation at Tesla, a company whose compensation philosophy has consistently awarded large one-time equity packages at significant career transitions rather than distributing equity more evenly across years. Elon Musk's own compensation — the subject of the largest and most litigated executive pay package in corporate history — has set a cultural norm at Tesla that equity awards can be of extraordinary magnitude.

The critical caveat, stated in the original data notes, is that Taneja's figure reflects a promotion-linked one-time award. One-time equity grants are a standard feature of executive compensation packages at technology companies, particularly at hiring or promotion events — they serve as a retention mechanism (options typically vest over 4 years with a 1-year cliff) and as a sign-on inducement that compensates a new executive for unvested equity forfeited at a prior employer. The grant-date fair value recorded in the proxy — approximately $278 million — is not cash received; it is the accounting value of options and restricted stock units whose actual realised value depends entirely on Tesla's share price over the vesting period.

At Tesla's 2024 share price, these options were significantly in the money, making the grant-date figure a reasonable approximation of expected value. But for context: if Tesla's shares had declined 30% from grant levels, the realised compensation would have been materially below the reported figure. The $48,767 hourly rate exists at the intersection of a large one-time award and a stock price that vindicated the grant's assumptions — a result that was not guaranteed when the board approved the compensation structure.

The Technology Premium: Why Tech CFOs Earn More

The concentration of top CFO hourly figures in technology companies — Alphabet, Microsoft, Amazon, Cisco, Meta, Netflix, NVIDIA, Apple — reflects a labour market reality that has been consistently documented in executive compensation research: the market for executive talent in technology companies, where the financial complexity and strategic stakes are highest and where the equity upside for investors (and therefore for executives) is largest, produces higher compensation than equivalent roles in non-technology industries. An Amazon CFO managing $590B in annual revenue across cloud, retail, advertising, and logistics operations in a company growing 10-12% annually faces genuinely different scope and complexity challenges than a CFO of an equivalent-revenue company in a slow-growth industry.

The technology sector's equity compensation premium also reflects the specific mechanism of startup-to-scale company culture: the equity grant norms established when these companies were growing hypergrowth businesses — where competitive talent required stock options that could be life-changing if the company succeeded — have persisted into the mega-cap era where the companies' total compensation budgets can accommodate equity packages that are extraordinary relative to any other industry's norms. Silicon Valley compensation culture, established when Apple and Google were competing for engineers in a genuinely competitive talent market, has created a precedent for executive equity that is now applied at scales that make the original competitive rationale difficult to sustain as the primary justification.

Amy Hood at $10,308/h: The CFO as Strategic Partner

Microsoft CFO Amy Hood's $10,308 per hour — third in the ranking and approximately $59M in annual total compensation — represents a different compensation model from Tesla's one-time promotion package. Hood has been Microsoft's CFO since 2013, making her one of the longest-tenured CFOs among the largest American companies. Her annual compensation has reflected sustained high performance at a company whose market capitalisation grew from approximately $250 billion when she became CFO to over $3 trillion in recent years — a 12× increase that created extraordinary returns for shareholders and, through equity grants and performance-based awards tied to those returns, for the executive team.

Hood's tenure and compensation arc illustrate the legitimate long-term incentive argument for equity-heavy CFO compensation: a CFO who receives equity grants tied to share price performance is theoretically aligned with shareholder interests in a way that a salaried CFO is not. If Microsoft's shares had stagnated, Hood's equity grants would have been worth far less than their grant-date fair value. The fact that Microsoft's shares rose dramatically over her tenure means the compensation appears large in retrospect; it would not have been guaranteed to be large when the equity was initially awarded. This is the theoretical underpinning of equity-based executive compensation — and Microsoft's return-to-shareholders during Hood's tenure is the empirical case study most often cited in its support.

Amy Hood has been Microsoft's CFO for over a decade as the company grew from $250 billion to $3 trillion in market cap. Her $10,308/h reflects both a large compensation package and a 12× shareholder return over which she presided. The alignment argument for equity compensation is rarely cleaner.

The Methodology's Limits: What the Hourly Rate Doesn't Show

The 55-hour work week assumption is a standardised calculation choice that produces comparability across the dataset but may not accurately represent the actual hours worked by CFOs of the world's largest companies. There is reasonable evidence that senior executives at major technology and financial companies routinely work in excess of 55 hours per week, particularly during earnings seasons, major transactions, or crisis periods. A CFO managing a major acquisition, an SEC investigation, or a significant capital raise may work 70-80 hour weeks for extended periods. If the actual hours are higher, the true hourly rate is correspondingly lower.

The more significant methodological limitation is the equity valuation issue. All compensation data reported to the SEC uses grant-date fair value for stock options and restricted stock units, computed using Black-Scholes or lattice option pricing models. These models produce reasonable expected-value estimates at the time of grant, but the actual cash equivalent the executive realises may be substantially higher or lower. A CFO who received $50M in options with a $200 strike price at grant, against a current share price of $180, has options worth zero — yet the proxy filing recorded $50M in compensation. A CFO whose options were granted at $200 against a current price of $350 has options worth more than the grant-date model projected.

The hourly figures are accounting constructs, not cash flows. They accurately represent the board's assessment of fair value at the time of grant and the SEC's required disclosure standard, but they do not represent a bank account balance. This distinction matters when comparing across companies and years, and it is why comparing the $48,767 Tesla figure to the $7,225 Apple figure requires acknowledging that both numbers are grant-date accounting entries whose realised value depends on subsequent stock price movements that had not yet occurred when the disclosures were filed.

End of Brief · Prism