THE 2025 ORDER BOOK

Prism · Aviation & Industry

Airbus · Boeing · 2025

THE 2025

ORDER

BOOK

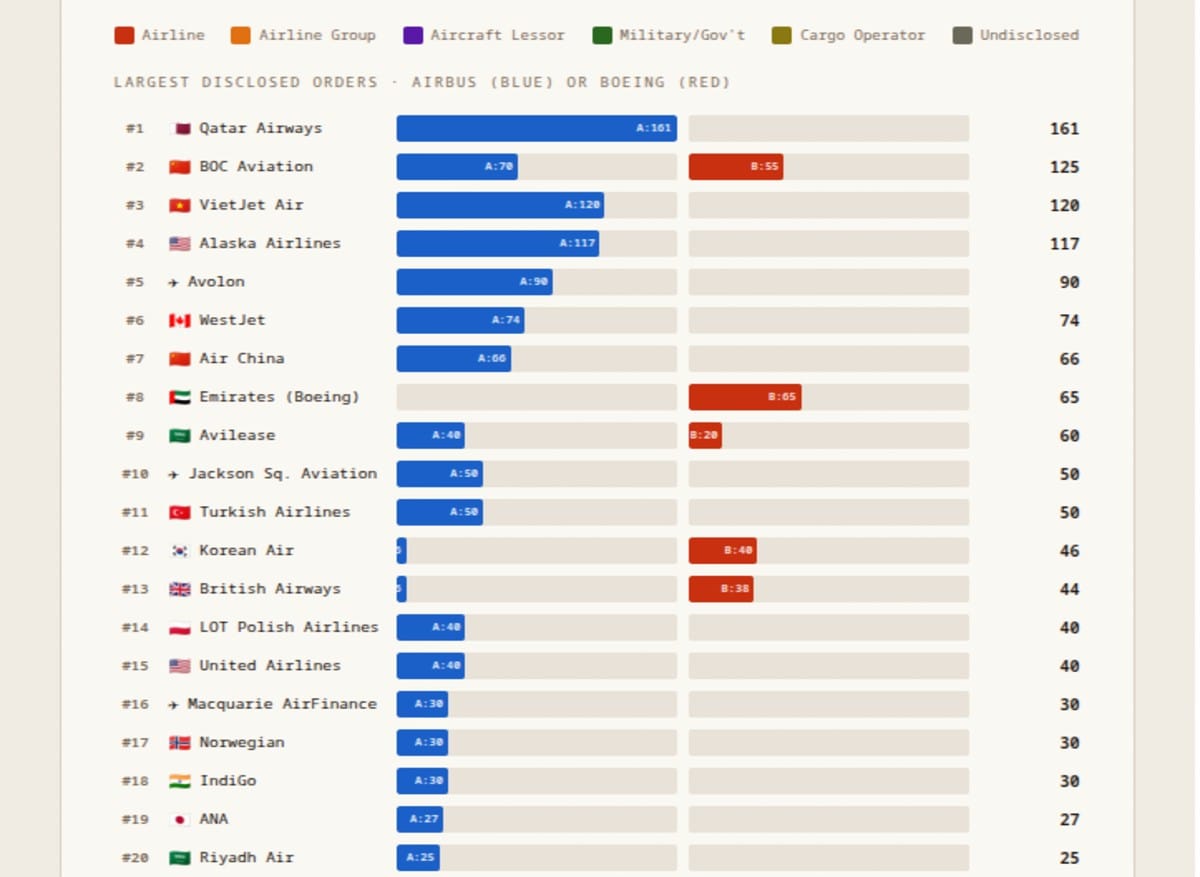

Qatar Airways ordered 161 aircraft — the largest single disclosed airline order of 2025. Alaska Airlines ordered 117. VietJet 120. The aircraft order book is a multi-hundred-billion-dollar ledger of confidence in air travel's future, denominated in units of narrowbodies and widebodies that will enter service in the late 2020s and early 2030s. Airbus took the majority of disclosed orders. Boeing — still rebuilding from the 737 MAX crisis and 2024 quality issues — secured significant but smaller share.

Metric: Aircraft orders placed with Airbus and Boeing · 2025 · by buyer category

Largest disclosed orders: Qatar Airways 161 (Airbus) · VietJet 120 (Airbus) · Alaska Airlines 117 (Airbus) · Avolon 90 (Airbus)

Undisclosed: 132 Airbus + 337 Boeing — largest single category for Boeing

Source: Airbus · Boeing · 2025

Largest disclosed orders: Qatar Airways 161 (Airbus) · VietJet 120 (Airbus) · Alaska Airlines 117 (Airbus) · Avolon 90 (Airbus)

Undisclosed: 132 Airbus + 337 Boeing — largest single category for Boeing

Source: Airbus · Boeing · 2025

Prism Desk·Sources: Airbus · Boeing·2025

Aircraft Orders 2025 · Airbus vs. Boeing · by Buyer Type and Airline

Hover rows for detail

Sources: Airbus · Boeing

Sources: Airbus · Boeing

Airbus — 2025 Order Highlights

✈ AIRBUS

Qatar 161 · VietJet 120 · Alaska 117

Avolon 90 · BOC Aviation 70

Air China 66 · WestJet 74

Avolon 90 · BOC Aviation 70

Air China 66 · WestJet 74

Boeing — 2025 Order Highlights

✈ BOEING

Undisclosed 337 (largest category)

BOC Aviation 55 · British Airways 38

Emirates 65 · Korea Air 40

BOC Aviation 55 · British Airways 38

Emirates 65 · Korea Air 40

"Undisclosed" buyers (132 Airbus · 337 Boeing) are customers whose identities are not publicly released at the time of order. This is standard industry practice — lessors placing speculative orders, airlines negotiating competitive contracts, or government purchasers requiring confidentiality all use undisclosed designations. Boeing's 337 undisclosed orders represent its largest single customer category — a structural feature of Boeing's order book that partially obscures the true demand picture for the 737 MAX family.

Airline

Airline Group

Aircraft Lessor

Military/Gov't

Cargo Operator

Undisclosed

Largest disclosed orders · Airbus (blue) or Boeing (red)

Airline LeadersQatar 161VietJet 120 · Alaska 117

WestJet 74 · Air China 66

Emirates 65 (Boeing)

WestJet 74 · Air China 66

Emirates 65 (Boeing)

Lessor ActivityAvolon 90BOC Aviation 70+55

Jackson Square 50

Macquarie 30 · CALC 30

Jackson Square 50

Macquarie 30 · CALC 30

Undisclosed469 totalAirbus 132 · Boeing 337

Boeing's largest category

Lessors + confidential buyers

Boeing's largest category

Lessors + confidential buyers

VietJet's 120-aircraft order is among the most strategically significant of the year. The Vietnamese low-cost carrier has emerged as one of Southeast Asia's most aggressive fleet expanders, betting on the continued growth of middle-class air travel in a region whose aviation penetration remains well below mature market levels. Southeast Asia — with 700 million people and rapidly growing middle classes — is the most contested battleground in global commercial aviation growth, and both Airbus and Boeing are competing intensely for fleet orders from carriers like VietJet, Lion Air, and Batik Air.

Source: Airbus · Boeing · 2025 orders data

161Qatar Airways

Largest Airline Order

Largest Airline Order

90Avolon

Largest Lessor

Largest Lessor

337Boeing Undisclosed

Largest Category

Largest Category

120VietJet

Southeast Asia Bet

Southeast Asia Bet

What an Aircraft Order Actually Buys

An aircraft order placed in 2025 is not a purchase in the conventional sense. It is a reservation — typically secured with a deposit, committed to a specific delivery slot in the manufacturer's production schedule, and governed by a purchase agreement that specifies the aircraft type, configuration, pricing escalation formula, and cancellation terms. Delivery lead times for narrowbody aircraft (737 MAX, A320 family) at both Boeing and Airbus are currently running 6-10 years for new orders, reflecting production backlogs that have accumulated from a combination of post-pandemic travel demand recovery, supply chain constraints, and Boeing's specific capacity challenges following the 737 MAX groundings and 2024 quality control issues. When Qatar Airways orders 161 aircraft in 2025, those aircraft will not enter service until the late 2020s and early 2030s at the earliest.

The order book serves multiple economic functions simultaneously. For the airline, it is a capital planning instrument — committing future cash flows to fleet renewal, securing preferred delivery positions in the production queue, and locking in (partially) the price escalation terms that will govern the final purchase price. For the aircraft manufacturer, it is a revenue visibility instrument — providing multi-year production planning confidence and the financial basis for plant investment and supplier commitments. For the aircraft lessors (Avolon at 90 aircraft, BOC Aviation at 70+55, Jackson Square at 50), it is a speculative inventory investment — ordering aircraft speculatively before identifying specific airline lessee customers, betting that delivery demand in 6-8 years will support profitable lease rates.

Qatar Airways orders 161 aircraft. They won't fly for years. The order book is not a purchase — it is a multi-decade supply chain commitment, a production queue reservation, and a bet on the future of air travel, denominated in narrowbodies and widebodies whose delivery dates are in the next decade.

Qatar Airways at 161: The Gulf Carrier's Long Game

Qatar Airways' 161-aircraft order is the largest single disclosed airline order of 2025 and reflects the carrier's strategic posture as one of the world's most aggressively expanding international carriers. Qatar Airways has built its network model around Doha's geographic position at the junction of Europe-Asia and Africa-Asia routes, using long-haul widebody aircraft (primarily A350 and 777 families) to connect cities that would otherwise require multiple connections. The 2025 order — heavily weighted toward Airbus products — continues a fleet expansion that was paused during the pandemic and the diplomatic crisis that led to Qatar's isolation by Saudi Arabia, UAE, Bahrain, and Egypt from 2017 to 2021.

The scale of Qatar's order also reflects the specific economics of state-backed carriers: Qatar Airways is owned by the Qatari government and operates with a mandate that includes both profitability targets and a strategic development function for Qatar's aviation and tourism sectors. The ability to make a 161-aircraft order commitment without the shareholder return pressure that constrains similar decisions at privately owned airlines reflects the specific advantages and specific accountability structures of government ownership. Qatar's order is a bet that global premium travel demand will grow, that Doha's hub position will be maintained, and that the A320-family narrowbodies in the order will find profitable employment on intra-Middle East and short-haul regional routes as the network fills in.

Alaska Airlines at 117: The Western US Consolidator

Alaska Airlines' 117-aircraft order reflects the carrier's strategic position as the dominant airline on the U.S. West Coast, following its 2016 acquisition of Virgin America and its ongoing integration of Hawaiian Airlines (acquired 2024). The fleet order is primarily directed at renewing and expanding the 737 MAX fleet that Alaska had ordered before and maintained through the MAX grounding period, plus additional narrowbody capacity for network expansion. Alaska's fleet strategy has historically been a source of competitive advantage — its single-type narrowbody fleet (737 series) generated pilot utilisation, maintenance, and parts commonality benefits that multi-type fleets cannot match.

The 117-aircraft figure also reflects the scale of Alaska's ambition in the post-pandemic competitive landscape: the COVID-19 period produced significant capacity consolidation as weaker carriers reduced fleets, and the carriers that survived with strong balance sheets have been aggressively ordering aircraft to lock in future capacity in markets where demand recovery has exceeded supply recovery. Alaska's 117-aircraft commitment is a declaration of intent to dominate its core markets and expand into new ones through the early 2030s. The timing — ordering in 2025 for 2029-2033 delivery — reflects Alaska's confidence that both leisure and business travel demand in the Pacific Northwest and West Coast markets will remain structurally above pre-pandemic levels.

VietJet at 120: The Southeast Asian Bet

VietJet Air's 120-aircraft order is the most strategically significant in terms of the long-term growth market it represents. Vietnam's aviation market has grown from negligible to significant in under two decades — VietJet itself was founded only in 2011 — and the country's 100 million population, rapidly expanding middle class, and geographical shape (1,650 km from north to south) create ideal conditions for low-cost air travel growth. VietJet has built its model on the ultra-low-cost carrier framework pioneered by Ryanair and AirAsia, using standardised A320 family aircraft, high utilisation, ancillary revenue, and route network density to offer prices that compete with train and bus alternatives on Vietnamese domestic routes.

The 120-aircraft order is a bet that this model — proven in Vietnam's domestic market — can be extended to international routes across Southeast Asia as the region's 700 million people continue to urbanise and as the cost of air travel continues to fall. Southeast Asia's aviation penetration rate (air trips per capita annually) remains well below European or American levels, and virtually all industry forecasts project it as the world's fastest-growing aviation market over the next two decades. The competition for Southeast Asian fleet orders between Airbus and Boeing reflects both manufacturers' recognition that capturing the region's growth will be critical to maintaining global market share in the decade ahead.

The Lessor Bloc: Avolon, BOC Aviation, and the Speculative Order

The aircraft lessor segment — Avolon at 90 aircraft (Airbus), BOC Aviation at 70 Airbus and 55 Boeing, Jackson Square Aviation at 50, Macquarie at 30, CALC at 30 — represents a collective order of over 300 aircraft placed by entities that do not themselves operate aircraft. Aircraft lessors are financial intermediaries who purchase aircraft from manufacturers, own them on their balance sheets, and lease them to airlines under operating or finance lease arrangements. The lessor model has become the dominant aircraft ownership structure in commercial aviation: approximately 50-55% of the global commercial aircraft fleet is now owned by lessors rather than by the airlines that fly it.

Lessor orders are structurally different from airline orders. An airline ordering aircraft is committing its own capital and operational plans to a specific fleet configuration. A lessor ordering aircraft is making a speculative investment in physical assets that it expects to be able to place with airlines globally at profitable lease rates when the aircraft deliver. The risk for lessors is that the market for specific aircraft types weakens between the order date and the delivery date — an obsolescence risk if a more fuel-efficient replacement type is announced, or a demand risk if a global recession reduces airline fleet expansion. The large lessor orders in 2025 reflect industry confidence that the 5-10 year delivery window will find active demand for narrowbody aircraft in a growing global aviation market.

Boeing's 337 Undisclosed: The Opacity Problem

Boeing's 337 undisclosed orders — the largest single category in its 2025 order book — represent both a standard industry practice and a specific challenge for Boeing's transparency with investors and analysts. Undisclosed orders are placed by buyers who request confidentiality at the time of announcement, typically for competitive reasons (an airline not wanting to reveal its fleet plans to competitors before finalising network strategies) or for pricing reasons (preserving negotiating leverage on final terms). Both Airbus and Boeing have significant undisclosed order backlogs at any given time.

What makes Boeing's 337 undisclosed orders notable is their disproportionate share of Boeing's total 2025 order count. When the largest identifiable customer category in Boeing's annual order book is anonymous, it limits the ability of analysts to assess the quality and distribution of Boeing's demand — are these long-haul widebody orders from established flag carriers? Short-haul narrowbody orders from lessor speculators? Government and military-adjacent purchases? The opacity matters because Boeing has been managing a genuine confidence deficit since the 737 MAX groundings of 2018-2019, the COVID-19 production disruptions, and the 2024 door-plug blowout incident that triggered additional regulatory scrutiny. A large undisclosed order book can reflect genuine strong demand, or it can reflect that customers prefer not to be publicly associated with Boeing orders during a period of reputational difficulty. The distinction matters for Boeing's strategic recovery, and the 2025 data alone does not resolve it.

End of Brief · Prism