SILVER'S FOUR GREAT RALLIES

Prism · Commodities & Markets

Macrotrends · Kitco · Amortization.org · 2026

SILVER'S

FOUR GREAT

RALLIES

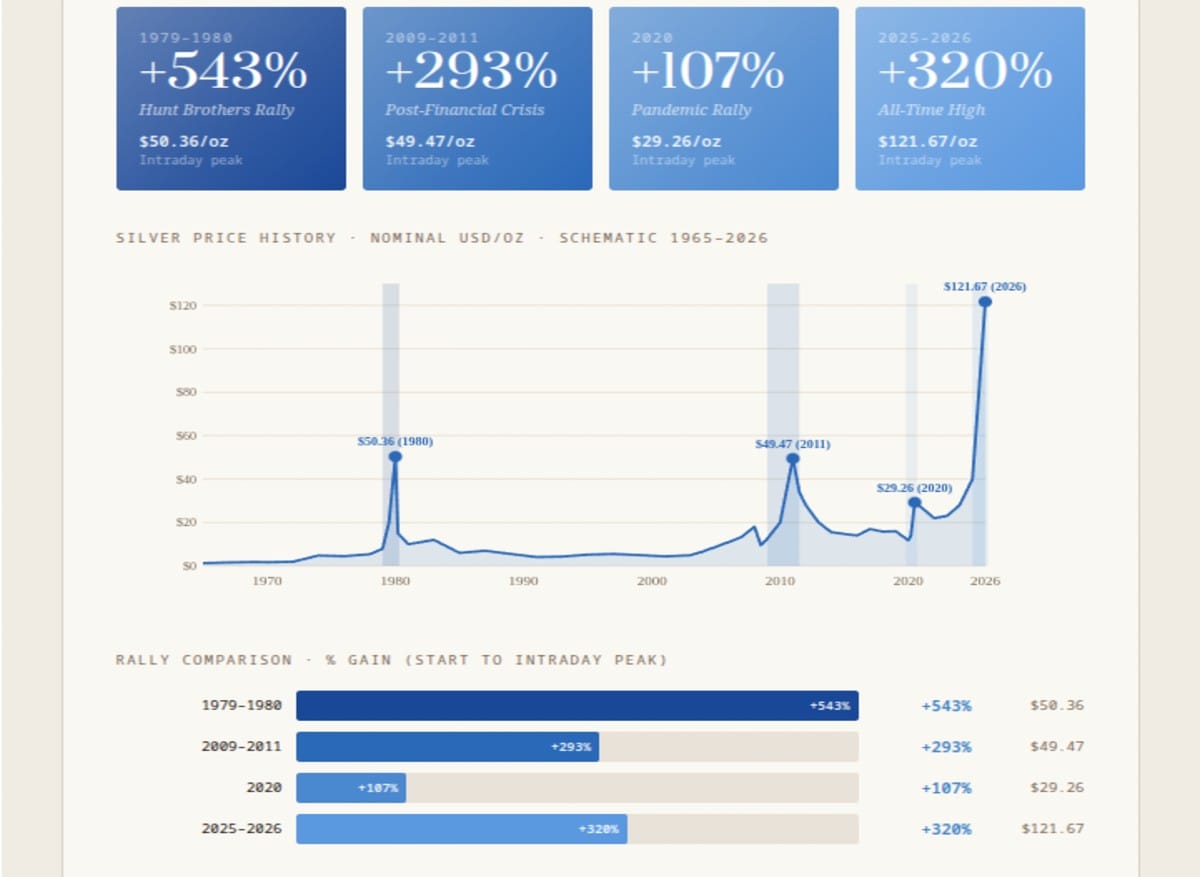

Silver has staged four extraordinary price rallies since 1965, each with a different cause but a consistent result: violent upside followed by brutal reversal. The 1979–1980 Hunt Brothers corner (+543%, peak $50.36) held the record for 45 years until the 2025–2026 rally surpassed it at $121.67. Each rally is a different story about why silver is not just a metal but a financial instrument with geopolitical and industrial dimensions.

Metric: Nominal USD/oz silver price · rally returns calculated from start to intraday peak

Note: Prices not adjusted for inflation · Current price as of February 2026

Rallies: 1979–80 +543% ($50.36) · 2009–11 +293% ($49.47) · 2020 +107% ($29.26) · 2025–26 +320% ($121.67 ATH)

Sources: Macrotrends · Kitco · Amortization.org

Note: Prices not adjusted for inflation · Current price as of February 2026

Rallies: 1979–80 +543% ($50.36) · 2009–11 +293% ($49.47) · 2020 +107% ($29.26) · 2025–26 +320% ($121.67 ATH)

Sources: Macrotrends · Kitco · Amortization.org

Prism Desk·Sources: Macrotrends · Kitco·Nominal USD/oz

Silver Price Rallies · Nominal USD/oz · 1965–2026

Hover rally cards for detail

Note: Nominal, not inflation-adjusted

Note: Nominal, not inflation-adjusted

Silver price history · nominal USD/oz · schematic 1965–2026

Rally comparison · % gain (start to intraday peak)

Industrial Demand Shift

Solar panels, EVs, and electronics now consume ~50% of annual silver production. Industrial demand has structurally displaced the price floor — unlike previous rallies driven purely by financial speculation.

Inflation Adjustment Note

In inflation-adjusted terms, the 1980 Hunt Brothers peak of $50.36 equals ~$200/oz in 2026 dollars. The current nominal ATH of $121.67 has NOT yet exceeded the real 1980 peak — a context often missing from coverage.

1979–80 Hunt Rally+543%Attempted market corner

One-third of global supply

CFTC intervention ended it

One-third of global supply

CFTC intervention ended it

2009–11 QE Rally+293%Post-GFC monetary stimulus

Inflation hedge demand

Near-matched Hunt peak

Inflation hedge demand

Near-matched Hunt peak

2025–26 ATH+320%Industrial + investment demand

$121.67 nominal ATH

Real 1980 peak still unbroken

$121.67 nominal ATH

Real 1980 peak still unbroken

⚠️ Inflation caveat: The 2025–26 nominal all-time high of $121.67 is frequently described as surpassing the 1980 Hunt Brothers peak. In real purchasing power terms this is not yet true. The $50.36 peak of January 1980 in 2026 dollars — adjusted for CPI inflation over 46 years — is approximately $190–210/oz depending on the deflator used. The 2026 nominal record is genuine; the real record from 1980 remains intact.

Sources: Macrotrends · Kitco · Amortization.org · Nominal USD/oz · Not inflation-adjusted · As of February 2 2026

+543%Hunt Brothers 1980

Largest Rally

Largest Rally

$121.672026 Nominal ATH

Current Record

Current Record

$50.361980 Nominal Peak

Held 45 Years

Held 45 Years

~$2001980 Peak Inflation

Adjusted (2026 $)

Adjusted (2026 $)

Why Silver Is Different From Gold

Silver occupies an unusual position in the landscape of investable assets — one that produces both its extraordinary return potential in certain regimes and its tendency toward violent, disorienting corrections. Unlike gold, which derives essentially all of its value from monetary and store-of-value functions (jewellery, central bank reserves, investment demand), silver has substantial industrial applications that consume approximately 50% of annual production. Solar panels, electronics, electric vehicles, medical devices, and antimicrobial applications create a structural industrial demand floor that gold does not have.

This dual nature — part monetary metal, part industrial commodity — means that silver responds to different catalysts than gold. Gold rallies on monetary debasement, geopolitical risk, and central bank demand. Silver rallies on all of those factors but also on industrial demand growth, supply constraints in mining, and the specific dynamics of the solar and EV industries. The result is a metal that, in the right regime confluence, can produce rally magnitudes that dwarf gold's returns — and in the wrong regime, can produce drawdowns that dwarf gold's corrections. The four major silver rallies since 1965 illustrate each distinct driver and the specific mechanism that eventually ended each run.

Silver is not gold. Gold is a monetary store of value with no significant industrial use. Silver is a monetary metal AND an industrial input. When both demand sets move simultaneously in the same direction, the results are extraordinary. When they diverge, the corrections are brutal.

1979–1980, +543%: The Hunt Brothers Corner

The 1979–1980 silver rally — +543% from approximately $7.90 to a peak of $50.36 per troy ounce on January 18, 1980 — remains the most dramatic commodity market manipulation in American financial history, and among the most dramatic in the history of any tradeable market. Nelson Bunker Hunt and William Herbert Hunt, sons of Texas oil billionaire H.L. Hunt, began accumulating silver futures and physical silver in the early 1970s, convinced that the abandonment of the gold standard in 1971 would produce catastrophic inflation and that silver offered the best protection. By late 1979, the Hunt brothers and their Saudi and Kuwaiti partners controlled an estimated 100-150 million troy ounces of silver — approximately one-third of global annual supply — through a combination of physical holdings and futures contracts.

The corner worked: as the Hunts continued to buy, other market participants and jewellery manufacturers facing a 10× price increase faced catastrophic losses on short positions and production costs. The panic was genuine. Silver jewellery manufacturers melted down antiques and family silverware to sell into the market. Restaurants replaced silver cutlery with stainless steel. The January 1980 peak of $50.36 was achieved in a market that had effectively lost normal pricing function.

The end came when the CFTC (Commodity Futures Trading Commission) and the Chicago Board of Trade changed the rules mid-game. In January 1980, the CBOT imposed "Silver Rule 7," which limited new long positions in silver futures and required existing holders to reduce positions — effectively forcing the Hunts to begin unwinding their accumulated positions. On March 27, 1980 — Silver Thursday — the Hunt brothers defaulted on $1.7 billion in margin calls. Silver fell 50% in four trading days. The Hunts subsequently filed for bankruptcy, paid $134 million to settle CFTC charges, and spent years in litigation. The 1980 crash demonstrated the regulatory response that inevitably follows market manipulation at scale: the rules change, the corner breaks, and the most leveraged participants are destroyed.

2009–2011, +293%: The Quantitative Easing Rally

The 2009–2011 silver rally — +293% from approximately $12.56 at the 2008 post-crisis nadir to a peak of $49.47 in April 2011 — was driven by an entirely different mechanism: the Federal Reserve's unprecedented monetary expansion following the global financial crisis. The first two rounds of quantitative easing (QE1 beginning November 2008, QE2 announced November 2010) dramatically expanded the Fed's balance sheet and created widespread expectations of inflation that drove investment demand for precious metals as currency debasement hedges.

Silver outperformed gold during this period — gold rose approximately 170% from trough to peak in the same timeframe, while silver's +293% reflected both the monetary hedge demand shared with gold and the growing investment thesis around silver's industrial demand growth in solar panels and electronics. The gold/silver ratio — which measures how many ounces of silver equal one ounce of gold — fell dramatically as silver outpaced gold, from approximately 80:1 at the 2008 crisis nadir to approximately 32:1 at the 2011 peak. The 2011 rally essentially restored silver to near nominal parity with its 1980 Hunt Brothers peak ($49.47 vs. $50.36) before a sharp correction pulled prices back toward $26-30 for most of the following decade.

The 2011 correction was initiated by a series of margin requirement increases at CME Group (the world's largest futures exchange) — five increases in eight trading days — that forced leveraged long holders to reduce positions. Unlike the 1980 CBOT rule changes, the 2011 margin increases were not targeted at any specific actor; they were presented as routine risk management responses to volatility. The effect was similar: forced position liquidation cascaded through the market, and silver fell from $49.47 to approximately $33 within two weeks.

Both the 1980 and 2011 silver peaks were ended by changes to exchange rules around futures margins — not by fundamental valuation changes. This is the recurring pattern: silver rallies on macro fundamentals, reaches extremes fuelled by leverage, and the end comes when the exchange changes the rules.

2020, +107%: The Pandemic Rally

The 2020 silver rally — +107% from approximately $14.10 in March 2020 to a peak of $29.26 in August 2020 — was the shortest and most structurally distinct of the four major rallies. The initial leg (March 2020) was a flight-to-safety compression: silver actually sold off sharply in the initial COVID-19 market panic as investors liquidated commodities to meet margin calls and raise cash, falling to $11.77 before recovering. The subsequent rally reflected the rapid deployment of unprecedented fiscal and monetary stimulus — the CARES Act, multiple rounds of stimulus payments, the Fed's zero interest rate commitment and expanded QE programme — that drove precious metals demand as inflation hedge assets.

The 2020 peak was short-lived: silver reached $29.26 in August 2020 and then consolidated for several months before a Reddit-driven retail investor squeeze attempt in early 2021 (the "WallStreetBets silver squeeze") briefly pushed prices toward $30. The squeeze failed — institutional silver shorts are primarily producers and processors hedging commercial exposure, not speculative shorts easily squeezed out — and silver retreated again. The 2020 rally demonstrated that in the era of commission-free retail trading, retail investor coordination could influence metals markets in the short term but could not overcome the structural reality of commercial hedger short positions.

2025–2026, +320%: The Industrial + Monetary Confluence

The 2025–2026 silver rally — +320% to a nominal all-time high of $121.67 — represents the first time that the two distinct demand drivers for silver (monetary/investment and industrial) have moved powerfully in the same direction simultaneously over a sustained period. Previous rallies were primarily monetary: the Hunt corner was manufactured supply scarcity, the 2009–2011 rally was inflation hedge demand, the 2020 rally was pandemic monetary stimulus. Each of these had significant industrial components, but industrial demand was not the primary driver.

The 2025–2026 rally combines: (1) continued monetary demand from inflation hedging and dollar debasement concerns as U.S. fiscal deficits remain structurally elevated; (2) the structural acceleration of silver industrial consumption from solar panel manufacturing, which by 2025 consumes approximately 15-20% of annual silver production alone, with EV and electronics demand adding further; (3) a supply deficit that has persisted for several years as new mine development has failed to keep pace with demand growth; and (4) geopolitical risk premiums related to U.S.-China trade tensions that affect the solar panel supply chain in which silver is a critical input.

The inflation-adjusted context is essential for understanding the 2026 rally's true historical position. The nominal all-time high of $121.67 is genuine — the first time silver has traded above its 1980 Hunt Brothers nominal peak of $50.36. But adjusted for CPI inflation over 46 years, the 1980 peak translates to approximately $190-210 in 2026 dollars. The 2026 rally has broken the nominal record by a wide margin but has not yet matched the real purchasing-power peak that the Hunt Brothers created in 1980. Whether the 2025–2026 rally extends further or follows the historical pattern of violent reversal is, at the time of this data, an open question rather than a settled outcome.

The Pattern Each Rally Shares

Four rallies across 60 years share a structural pattern that is worth identifying explicitly. Each begins with a genuine fundamental driver: monetary panic (1979), QE-driven inflation expectations (2009), pandemic monetary stimulus (2020), industrial demand confluence (2025). Each is amplified by leverage — futures positions, leveraged ETFs, margin accounts — that translates the fundamental signal into a price move of a magnitude far exceeding what fundamental valuation analysis would predict. And each ends, not when the fundamental driver reverses, but when the leverage becomes unsustainable and the exchange or regulatory environment changes the rules: Silver Rule 7 in 1980, CME margin increases in 2011, the collapse of the Reddit short squeeze in 2021.

The implication for investors is significant and sobering: in silver, you can be right about the fundamental thesis and still lose money if you are levered and the timing is wrong. The 1980 crash did not happen because the Hunts were wrong that inflation was a threat — inflation was severe and genuine in 1980. It happened because they were the wrong kind of right, right through leverage that made them dependent on the continued willingness of exchange authorities to allow the position to persist, and that willingness ended abruptly. Silver's history is a lesson in the difference between being right about the macro thesis and being right about the tradeable instrument — a difference that has cost many silver bulls their capital even in the years when their fundamental analysis was vindicated.

End of Brief · Prism