GLOBAL COPPER PRODUCTION 2000–2024

Prism · Resources & Geopolitics

USGS · 2000–2024

COPPER

PRODUCTION

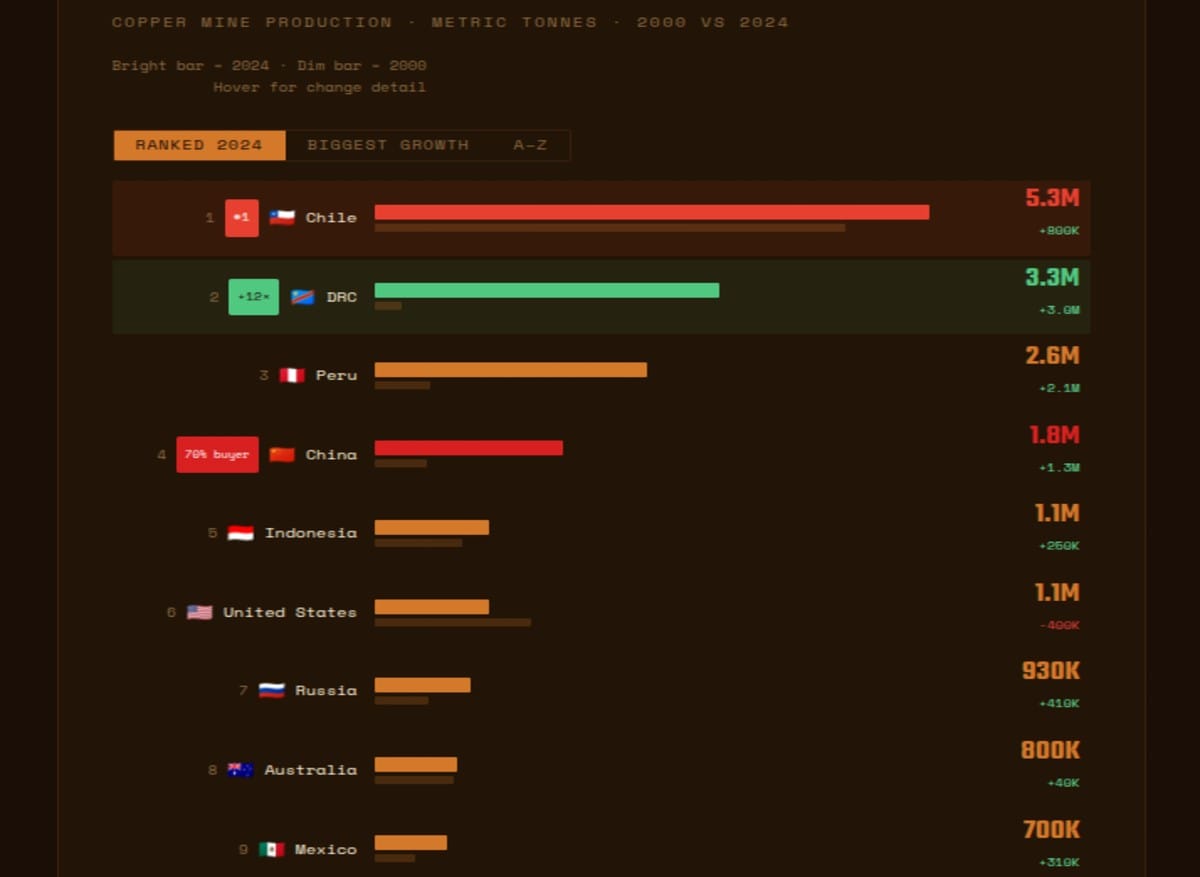

2000–2024 Chile still leads. The DRC has surged 12×. China buys 70% of Peru's output and controls 70% of DRC mines. The copper supply chain is the physical foundation of the energy transition — and China has positioned itself at its centre.

Metric: Copper mine production · Metric tonnes · 2000 vs 2024

Includes all copper extracted before smelting/refining

Source: U.S. Geological Survey (USGS)

Includes all copper extracted before smelting/refining

Source: U.S. Geological Survey (USGS)

🇨🇳 China's copper control strategy:

• Buys ~70% of Peru's copper output — largest single buyer in most supplier nations

• Chinese companies control 70%+ of DRC copper mines (since ~2015)

• ~55% of global refined copper demand · Refines ~40% of global copper despite producing only ~8% of mine output

• Buys ~70% of Peru's copper output — largest single buyer in most supplier nations

• Chinese companies control 70%+ of DRC copper mines (since ~2015)

• ~55% of global refined copper demand · Refines ~40% of global copper despite producing only ~8% of mine output

Copper Mine Production · Metric Tonnes · 2000 vs 2024

Bright bar = 2024 · Dim bar = 2000

Hover for change detail

Hover for change detail

DRC: Fastest Rise

+3.04M

260K in 2000 → 3.3M in 2024 · 12× growth

Chinese capital funded the entire surge

Chinese capital funded the entire surge

China buys

70%

Of Peru's copper output · Near-monopsony buyer power · Shapes supplier foreign policy

Source: U.S. Geological Survey (USGS) · Mine production in metric tonnes · 2000 and 2024

5.3MChile 2024

#1 Producer

#1 Producer

3.3MDRC 2024

12× Growth

12× Growth

~55%China's Share

Global Cu Demand

Global Cu Demand

22M+Total Global

Production 2024

Production 2024

Why Copper Is the Metal of the Energy Transition

Copper is the critical material of the clean energy transition. An electric vehicle requires 3–4 times as much copper as an internal combustion engine vehicle. A wind turbine needs roughly 4–5 tonnes of copper per megawatt of capacity. Solar installations, grid-scale batteries, EV charging infrastructure, and high-voltage transmission lines all require substantial copper — and the net-zero scenarios require a dramatic increase in global copper production that analysts increasingly describe as one of the most constrained bottlenecks in the decarbonisation timeline. Global copper mine production has grown from approximately 13.5 million tonnes in 2000 to over 22 million tonnes in 2024 — a 63% increase in 24 years. But demand growth driven by electrification may require another 50–100% increase before 2050, requiring extraordinary mine development in an industry where average discovery-to-production time is 16–17 years. The copper supply constraint is not a temporary disruption — it is a structural bottleneck that will shape the pace and cost of the energy transition for decades.

Chile still dominates copper production. But China dominates copper economics — controlling 70% of DRC mines, buying 70% of Peru's output, refining 40% of global copper. The energy transition runs through Beijing's supply chain decisions.

Chile at 5.3M: Irreplaceable But Challenged

Chile's production has declined slightly from its 2007 peak of ~5.8M tonnes. Escondida — the world's largest copper mine — faces declining ore grades requiring progressively more energy and water to maintain output. Water scarcity in the Atacama Desert increasingly constrains expansion in a region where mines and communities compete for a diminishing resource. Political uncertainty around mining royalties and the state copper company Codelco's significant capital cost overruns at expansion projects add further headwinds. Chile remains irreplaceable in the short term but its trajectory raises real questions about medium-term production capacity without major new mine development.

The DRC's 12× Rise: Chinese Capital, African Copper

The Democratic Republic of Congo's transformation from 260,000 tonnes in 2000 to 3.3 million tonnes in 2024 is the most remarkable production growth story in modern mining. The Katanga Copper Belt holds some of the world's highest-grade remaining ore bodies, and their development has been financed overwhelmingly by Chinese state-owned enterprises — CMOC, Zijin Mining, and others. Chinese companies' control of over 70% of DRC copper mines by the mid-2010s reflects deliberate industrial strategy that long predates the clean energy transition narrative. DRC copper ore flows overwhelmingly to Chinese smelters, contributing to China's position processing ~40% of global refined copper despite producing only 8% of mine output. China owns the upstream extraction while consuming the downstream product, capturing value at both ends of the chain — a structural position that took twenty years to build and will not be quickly dislodged.

Peru at 2.6M: The 70% Dependency

Peru's growth from 530K to 2.6M tonnes represents a major development success driven by investments at Antamina, Las Bambas, Cerro Verde, and others. But China buying approximately 70% of Peru's copper output creates a dependency that shapes Lima's foreign policy latitude toward Beijing. Chinese companies own Las Bambas — one of Peru's largest mines — and its periodic community-driven road blockades disrupting production preview the political risk that affects many high-potential copper development zones globally. The mine community opposition dynamic, where local populations feel excluded from resource revenues, is a risk factor copper supply projections consistently underweight in their production forecasts.

The United States at 1.1M: A Strategic Deficit

U.S. production has declined from 1.5M tonnes in 2000 to 1.1M in 2024 — one of the few major producers with falling output. The Resolution Copper project in Arizona, potentially one of the world's largest deposits, has been in permitting discussions for over two decades without reaching production. Average U.S. mine permitting timelines are 7–10 years versus 2–3 years in Chile and Australia. The irony is acute: the United States mandates and subsidises a clean energy transition requiring enormous copper quantities while making domestic mine development extraordinarily difficult. This regulatory asymmetry ensures copper is produced in Chile, Peru, and the DRC and processed in China rather than America — shifting geopolitical supply chain control toward actors whose strategic alignment with American interests ranges from complicated to adversarial.

India's Copper Dependency: A Strategic Vulnerability

India is absent from the list of significant copper producers despite its large and growing economy. Domestic copper mining is minimal — the Hindalco and Vedanta operations process imported concentrate — and the 2018 closure of the Sterlite/Vedanta smelter in Thoothukudi following pollution protests removed significant refining capacity at exactly the wrong moment in the energy transition timeline. India's copper imports will intensify as its electrification drive accelerates. EV targets, solar installation mandates, and grid modernisation all imply dramatic demand increases that India has no realistic prospect of meeting domestically. India will need to be a strategic copper buyer in markets where China exercises near-monopsonistic pricing influence — buying in markets China already dominates, on terms China substantially controls.

India's clean energy transition depends on securing copper supply chains currently controlled by its primary strategic competitor. This is not merely a procurement challenge — it is a strategic vulnerability requiring the same policy seriousness applied to oil supply security. India has a critical minerals policy in development, and strategic investments in copper mines in Chile, Peru, Zambia, and Australia are being pursued by Indian companies. Whether the pace and scale of these investments matches the urgency of the supply constraint is the open question. The countries that secure long-term copper offtake agreements in the next five years will be better positioned for the energy transition of the 2030s and 2040s. Those that arrive late will pay China's price.

End of Brief · Prism