Critical Minerals in U.S. Mining Waste

Prism · Mining & Critical Resources

Critical Minerals

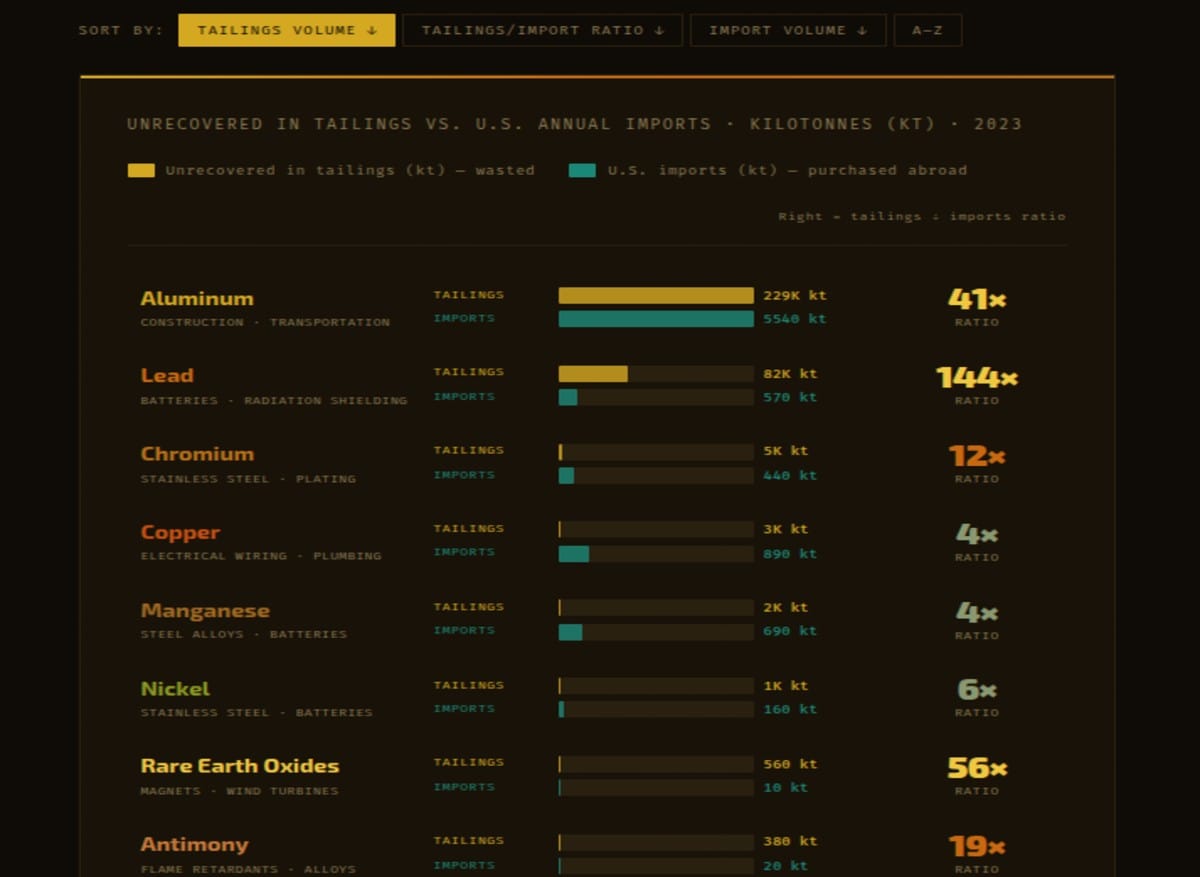

in U.S. Mining Waste U.S. hard-rock mines sent 229,430 kilotonnes of aluminium to tailings piles in 2023 — while importing 5,540 kilotonnes. Millions of tonnes of critical minerals sit unrecovered in waste heaps across federal land, as the nation pays for imports of the same materials.

in U.S. Mining Waste U.S. hard-rock mines sent 229,430 kilotonnes of aluminium to tailings piles in 2023 — while importing 5,540 kilotonnes. Millions of tonnes of critical minerals sit unrecovered in waste heaps across federal land, as the nation pays for imports of the same materials.

229K kt

Aluminium in tailings 2023

~10

Minerals tracked in waste

56×

Rare earths: tailings vs imports

What are tailings? Mining waste — called tailings — is the material left over after the target mineral has been extracted from ore. Because extraction processes are imperfect and economically selective, tailings often contain significant quantities of other valuable minerals that were not the primary extraction target. These unrecovered materials accumulate in tailings ponds and waste heaps near mine sites, often on federal land.

Sort by:

Unrecovered in Tailings vs. U.S. Annual Imports · Kilotonnes (kt) · 2023

Source: Elizabeth Holley, Colorado School of Mines, USGS · 2023 hard-rock mine tailings on U.S. federal land · Figures include main-product output

Unrecovered in tailings (kt) — wasted

U.S. imports (kt) — purchased abroad

Right = tailings ÷ imports ratio

229K kt

Aluminium

Wasted in tailings vs 5,540 kt imported — 41× ratio

Wasted in tailings vs 5,540 kt imported — 41× ratio

56×

Rare Earths

560 kt wasted vs 10 kt imported — highest ratio

560 kt wasted vs 10 kt imported — highest ratio

28×

Cobalt

280 kt wasted vs 10 kt imported — EV battery critical

280 kt wasted vs 10 kt imported — EV battery critical

30×

Lithium

90 kt wasted vs 3 kt imported — at ratio of 30×

90 kt wasted vs 3 kt imported — at ratio of 30×

The Tailings Paradox

The United States is simultaneously one of the world's largest mineral importers and one of the world's largest generators of mineral-bearing waste. U.S. hard-rock mines on federal land sent approximately 229,430 kilotonnes of aluminium-bearing material to tailings piles in 2023 — while the nation imported 5,540 kilotonnes of aluminium. For rare earth elements, the disparity is even more striking: 560 kilotonnes of rare earth oxide-bearing material discarded as waste versus 10 kilotonnes imported from abroad, a ratio of 56 to 1. The critical mineral that US policymakers have identified as the central vulnerability of the national security supply chain is sitting in waste piles on federal land at 56 times the annual import volume.

The existence of this paradox does not mean that recovering these minerals from tailings is straightforward or economically viable under current conditions. Tailings are not ore — they are the material that was left after the economically viable mineral extraction was completed. The concentration of critical minerals in tailings is typically lower than in primary ore, which means extraction costs per unit are higher. The mineralogical form of the minerals in tailings may also differ from primary ore, potentially requiring different processing chemistry. But the scale of the opportunity — particularly given the national security premium that US policy has placed on domestic critical mineral supply — means that tailings reprocessing deserves serious economic and technological evaluation that it has historically not received.

The U.S. designates rare earth elements as critical national security minerals, imposes tariffs on Chinese rare earth imports, and funds programs to diversify rare earth supply — while discarding 560 kilotonnes of rare earth-bearing material to waste piles annually. The strategic incoherence is significant.

Cobalt and Lithium: The Battery Supply Chain Problem

The cobalt and lithium data in this dataset are particularly consequential given the central role of both minerals in electric vehicle battery manufacturing — the technology around which the US Inflation Reduction Act's $370 billion clean energy investment was structured. The IRA's domestic content requirements explicitly aim to shift lithium-ion battery supply chains toward US and allied sources, reducing dependence on Chinese-controlled cobalt from the Democratic Republic of Congo and Chinese-processed lithium from South America. The data shows that U.S. mines are discarding 280 kilotonnes of cobalt-bearing material and 90 kilotonnes of lithium-bearing material annually as tailings — at import ratios of 28 and 30 to 1 respectively. The minerals that battery manufacturers are scrambling to source from abroad are present in domestic mine waste at multiples of current import volumes.

The cobalt situation is particularly striking. The Democratic Republic of Congo accounts for approximately 70% of global cobalt production, and cobalt mining in the DRC has been extensively documented for child labour, unsafe conditions, and environmental damage. The US policy position — subsidising EV manufacturing through the IRA while sourcing cobalt from DRC operations — has been a persistent tension in clean energy policy. The availability of cobalt in domestic tailings at 28 times annual import volumes creates a policy-coherent alternative: reprocessing domestic mine waste would simultaneously reduce import dependence, reduce supply chain exposure to DRC conditions, and utilise material that is already disturbed rather than opening new mine footprints.

The Technology of Tailings Reprocessing

Tailings reprocessing is not a theoretical concept — it has been practised commercially in several contexts. The Witwatersrand gold tailings dumps in South Africa have been systematically reprocessed to recover gold and uranium using improved extraction techniques unavailable at the time of original mining. Several copper operations have reprocessed their own tailings as copper prices rose and processing technology improved. The economics of tailings reprocessing depend on three variables: the concentration and mineralogical accessibility of the target minerals, the cost of reprocessing per tonne of material, and the market price of the recovered minerals. The current policy environment — elevated critical mineral prices driven by EV demand and national security premiums, combined with IRA production tax credits for domestic critical mineral production — has significantly improved the economic case for tailings reprocessing that was not viable under prior market conditions.

Several startups and established mining companies are actively developing tailings reprocessing programmes targeting battery metals. Lithium Americas, Piedmont Lithium, and others have examined lithium recovery from domestic tailings. The Department of Energy has funded research programmes on tailings reprocessing through the Critical Materials Institute. The regulatory framework for tailings reprocessing on federal land remains underdeveloped — it is unclear whether reprocessing existing tailings requires the same permitting as opening a new mine, which would impose years-long delays and costs that could make otherwise viable projects uneconomic. Clarifying the regulatory pathway for tailings reprocessing is arguably the single most important near-term policy action available to accelerate domestic critical mineral supply.

What the Data Doesn't Show

The USGS/Colorado School of Mines dataset underlying this analysis captures material sent to tailings from U.S. hard-rock metal mines on federal land — a subset of total U.S. mining activity. Coal mines, phosphate mines, and private-land hard-rock mines are not captured. The figures represent the total mass of material in tailings that contains the mineral in question, not a direct measurement of economically recoverable mineral content. The gap between "material containing mineral X in tailings" and "economically recoverable mineral X from tailings" is the critical unknown that only detailed geological and metallurgical characterisation of specific tailings deposits can resolve. The national-level figures in this dataset are a measure of the scale of the opportunity, not a bill of recoverable materials. But they are large enough — particularly for rare earths, cobalt, and lithium — to justify the characterisation work that would determine exactly how much is actually recoverable.

End of Brief · Prism